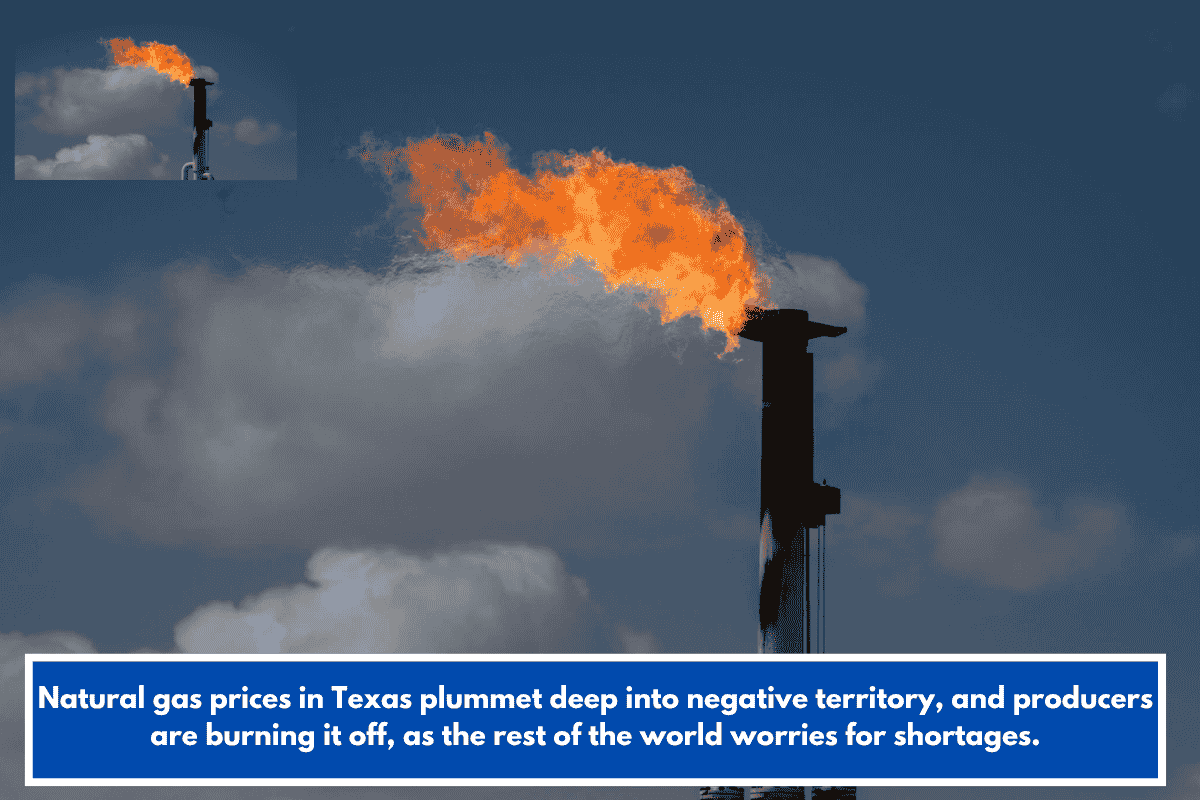

In the Permian Basin’s Waha hub, natural gas prices dropped to a record low of -$9.75 per million BTUs last week, with forecasts of -$10 soon due to pipeline maintenance. This happens because drilling for oil produces excess gas, but limited pipelines cause bottlenecks. Producers often flare (burn off) the surplus—flaring is at five-year highs—rather than pay to dispose of it. Despite this, drillers keep producing since oil prices have surged 47% to nearly $100/barrel amid the U.S.-Israel war on Iran, making operations profitable overall.

Global Shortages and Price Spikes

The war has flipped the script elsewhere. Iran retaliated by closing the Strait of Hormuz (20% of global oil and LNG flows) and attacking Qatar’s Ras Laffan facility, sidelining 17% of Qatar’s LNG exports for up to five years. This hits Europe and Asia hard:

- Europe: Benchmark futures leaped 35% to 70 euros/MWh (~$20/million BTUs), double pre-war levels. With low winter stockpiles, summer restocking looms as a crisis—far from 2022’s 345 euros peak, but still painful.

- Asia: Spot LNG prices could hit $30/million BTUs this summer (from $26 now) or $40 in six months if the strait stays shut. Nations are rationing: four-day workweeks, work-from-home mandates, and coal revivals (e.g., Thailand at full capacity, Bangladesh boosting use). South Korea and Taiwan—key semiconductor makers—are prepping more coal reliance.

Why the Divide?

It’s a classic supply mismatch. U.S. shale booms create local oversupply without enough gas export pipes, while war disrupts Middle East chokepoints, forcing Europe/Asia to bid up scarce LNG. No quick fix: Permian needs infrastructure; global markets need Strait reopening or repairs.

For context, imagine gas as water: West Texas has bursting pipes flooding the basement (-prices), while Europe/Asia face drought (skyrocketing bids). This volatility could slow economies, hike energy bills, and shift Asia back to dirtier fuels. What’s your take on how this might affect India or cricket season power needs?